")

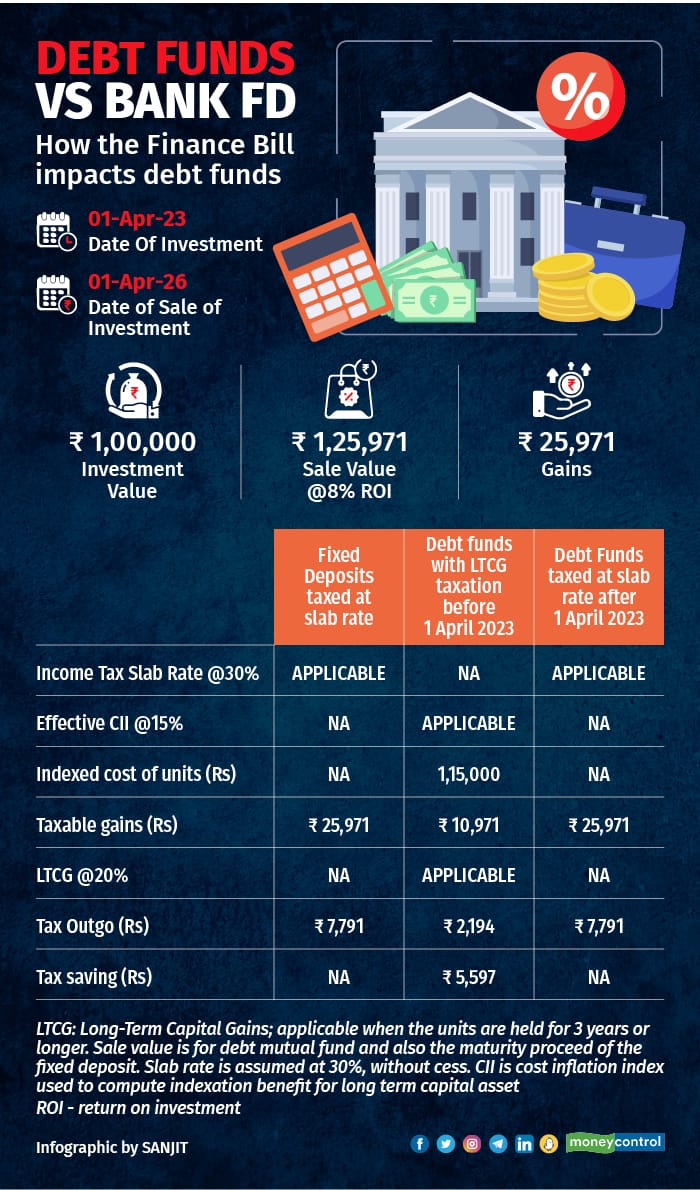

With the Lok Sabha passing the Finance Bill, 2023 with 64 official amendments on March 24, 2023, any gain (irrespective of the holding period) from debt funds and exchange-traded funds (ETFs), international funds, gold funds and certain categories of hybrid funds will now be taxed at your income-tax rates (or the slab rate). In other words, long-term capital gains tax benefits, along with indexation benefits, are abolished.

This comes into effect from April 1, 2023. The Bill awaits Rajya Sabha approval and President’s assent, but experts say that is just a formality.

Debt funds, FDs, bonds: Who’s the fairest of them all?

Currently, any capital gain on redemption of a debt fund held for three years or longer is treated as long-term capital gain and is taxed at a flat 20 percent with indexation benefit. Any capital gain on redemption before three years is treated as short-term capital gain and is taxed at an individual’s income tax slab rate. This makes them an attractive post-tax option for long-term investors in the higher income tax brackets compared to fixed deposits (FDs) and bonds. Interest income from FDs and bonds is taxed at an individual’s income tax slab rate.

Also read: Indexation benefits on debt funds will go away now

Following the latest change, this differentiation in debt fund taxation ― for a holding period of under three years, and of three years or longer years ― will no longer hold. Any capital gain on redemption of debt funds bought on or after April 1, 2023, will be taxed at your income tax slab rate. A small consolation here: your gains on any investments made until March 31, 2023, will be grand-fathered.

With the tax arbitrage between debt funds (capital gains) on one hand, and bonds and FDs (interest income) on the other, gone, the three are now at par from a taxation perspective.

The amendment to the Finance Bill has put debt funds on par with bank fixed deposits

The amendment to the Finance Bill has put debt funds on par with bank fixed deposits

In addition to the taxation of interest, listed bonds also attract capital gains tax. Short-term capital gains (holding period of up to one year) from listed bonds are taxed at your income tax slab rate. Long-term capital gains are taxed at 10 percent without indexation. But as Joydeep Sen, Corporate Trainer-Debt, points out, in the context of bonds, it is the coupon (interest) rather than the capital gain that is a more important source of income.

He says, “As the tax treatment of capital gains on debt mutual fund units comes at par with that of interest received on bonds, investors may start evaluating good quality bonds, subject to liquidity in the secondary market.” Most savvy investors value the assured liquidity that debt mutual funds offer. Since not many bonds trade at their fair value in the secondary market, in many instances investors have routed their fixed-income investments through mutual funds. Going forward, the taxation change may drive some to bank FDs and good-quality bonds.

Furthermore, compared to FDs, debt funds can help you postpone your tax liability. Mihir Tanna, Associate Director, SK Patodia and Associates, says that though individual investors have the option to offer the interest income for taxation purposes on a receipt basis or on an accrual basis, most prefer to get taxed on an accrual basis. This is because the TDS on interest gets deducted each year and it is an administrative hassle to carry forward the TDS till the time of maturity of the bond. Also, accrual-based taxation helps avoid the possibility of inquiry from the income tax department for a mismatch of data reported to the income tax department and income offered to tax. Compared to this, gain on investments in units of debt funds are taxed only after they are sold. According to him, debt fund investments thus can help long-term investors postpone their liability.

So, though it is still appealing to use debt funds to keep postponing the tax liability to your golden years when the income is relatively low, it must be noted that the gains will still get taxed as per the slab rate. Earlier, the indexation benefit was used to bring down the tax liability substantially for such investors. “In a low-yield asset class such as fixed income, denying indexation benefit kills the idea of long-term tax-efficient compounding,” says a senior fund manager who is not authorised to speak to the media.

Gautum Nayak, Partner, CNK & Associates, makes an interesting point in the context of the set-off of capital loss in debt funds. He says, “With indexation benefit, till now debt MF investors were able to show capital loss without any actual loss thereby saving on tax. Once the indexation benefit goes, unless your debt investments have an actual capital loss, you cannot use it for set-off against capital gains in another asset.” He further adds, “While you can set off a capital loss in debt funds against capital gains in other assets, most investors do not make a capital loss in debt funds unless there is a credit event resulting in loss of capital.”

From the perspective of ease of any time of withdrawal, debt mutual funds continue to score over FDs. Premature withdrawals from FDs attract a penal rate of interest. Some debt funds have an exit load, but for very short periods.

Also read: Not just debt funds – gold and international funds to also lose from Finance Bill amendment

Should you sell your debt funds?

Does the recent amendment imply that investors will shift from debt funds to FDs?

According to Niranjan Avasthi, Head - Product, Marketing and Digital Business, Edelweiss AMC, thanks to their higher yields, debt mutual funds like liquid, overnight and low-duration funds still remain reasonably attractive compared to other short-term investment avenues. He adds, “In the coming years, incremental flows in medium- to long-term debt mutual funds might get impacted due to this change.”

Gautam Kalia, Head - Investment Solutions, Sharekhan, says, “No new investors are expected to switch to debt mutual funds from fixed deposits hereafter. The withdrawal of indexation benefit and the possibility of mark-to-market losses make debt funds a less attractive bet for most conservative investors, compared to fixed deposits.”

Note that existing investments in debt funds, international funds, gold funds, etc. and even new investments made in them until March 31, 2023, will not be affected by this change. These funds will continue to enjoy the favourable long-term capital gains tax as before.

Bond markets

Commenting on the development, Sandeep Jethwani, Co-founder of Dezerv, says that the intent seems to be to align all the different investment options in fixed income to a common tax structure. There have been changes in market-linked debentures (MLDs), insurance policies, and now finally, debt mutual funds. In doing so, the differential benefits available to larger investors have been done away with. Also, this will make capital-raising easier for banks.

Offering a different view, Joydeep Sen says that while investment in equity stocks and mutual funds should be incentivised, bonds/debt funds are equally important from a resources point of view. The government should treat the two asset classes equally for the long-term development of the bond market.

For now, debt funds have lost their tax advantage. It’s over to the fund managers now to get back to the drawing board and dig deeper to earn that higher return.

Also read: March 31 deadline for MF nomination gives headache to investors